In this week, the Treasury market got a fair amount of new information, both in the form of economic data, as well as a better sense of investors response function to recent developments.

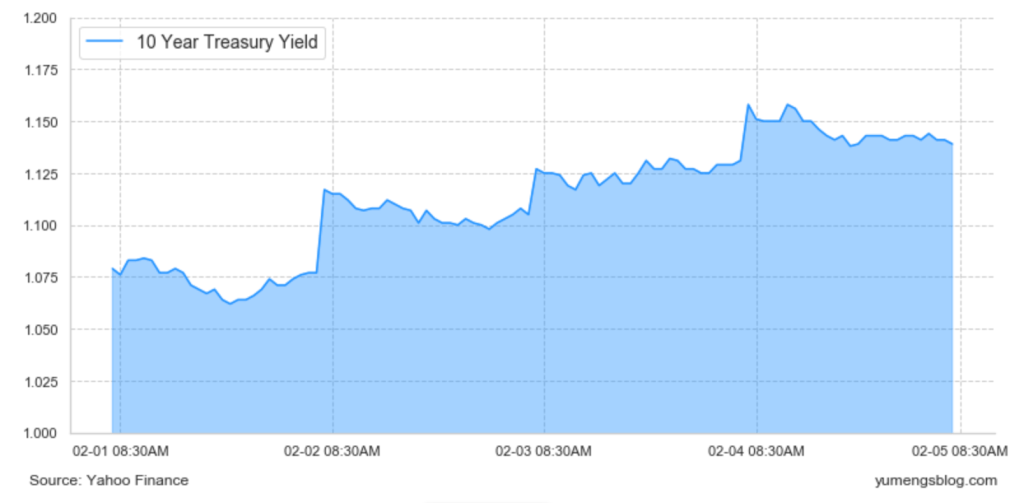

As mentioned in the last blog, Friday’s CPI print was the most attention-gasping fundamental event of the week. We saw a slightly above expectations headline print, but the core number came in as expected, increasing five tenths of a percent month over month. This pace of inflation, while certainly above trend, wasn’t enough to get the market truly concerned about inflation getting out of the Feds control. So one should see a fairly impressive flattening into the release but the generally as expected print actually gave way to a little bit of a steepening. My interpretation would be that besides the biggest fundamental event of the week i.e. the CPI release, the fact that the 30 year auction tailed more than three basis points actually led to the most dramatic price action. So the long end of the curve cheapened up into the auction, which contributed meaningfully to the fives thirties re-steepening.

Future Path of Inflation

While Powell has retired the transitory characterization of inflation, as we think about the path of inflation throughout 2022, it is worth mentioning that the factors that originally led to transitory are still going to be in place. The supply chain issues and pandemic specific increases in prices are still going to work themselves out. As the Fed has said, it’s just taken longer than was initially presumed. Taking this fact, combined with the Fed that’s leaning hawkishly and prepared to offset inflation from the demand side, it’s going to be difficult to see an acceleration in realized prices and also inflation expectations as we start to get through the first half of next year.

As Biden’s recent comments right before the release, the decline in energy prices associated with the release of oil from the strategic petroleum reserves, wouldn’t be reflected in November CPI, and that’s precisely what we saw. A slightly higher than expected headline figure that was driven by elevated energy costs. Biden also noted that the expected moderation in the pace of car prices wouldn’t show up in the data, and again, he was correct. Easy to forecast when you have the numbers ahead of time. What we saw in practical terms was a slowing, but a still meaningful contribution from new and used auto prices to the core CPI print. But to his point, there is downward pressure on energy prices that will eventually work its way through to the inflation data.

And let us not forget the importance of the base effects that come into play in 2022. Effectively a reversal of Q2 2021 i.e. the bar is now much higher for the year over year pace of inflation to continue to accelerate during the months of April, May and June of next year. This is something that the Fed has referenced directly in the past and I suspect that even though the transitory language has been retired, the reality is that the Fed would like to see those numbers before they make any decision related to rate hikes. The nuance of this timing implies that it will be very difficult to justify pricing in a March rate hike.

These bring us back to one of the primary debates in the market at this moment and that is the flattener versus the steepener. I would lean to the flattening side, working under the assumption that anything that brings forward rate hikes or implies a higher terminal rate will ultimately hurt twos, threes, and fives more than tens and thirties. But the most important is not to rule out other possibilities. For now the only way to envision a sustainable steepener is if one of two things occurs. First, the Fed signals an unwillingness to address higher than expected consumer prices and the second being that the market loses faith in the Fed’s ability rather than willingness to combat accelerating inflation. At the end of the day, again, either of those would be my base case scenario, but I won’t be surprised to see episodes of re-steepening if the realized inflation data continues to outperform expectations as it did in the second quarter of 2021.