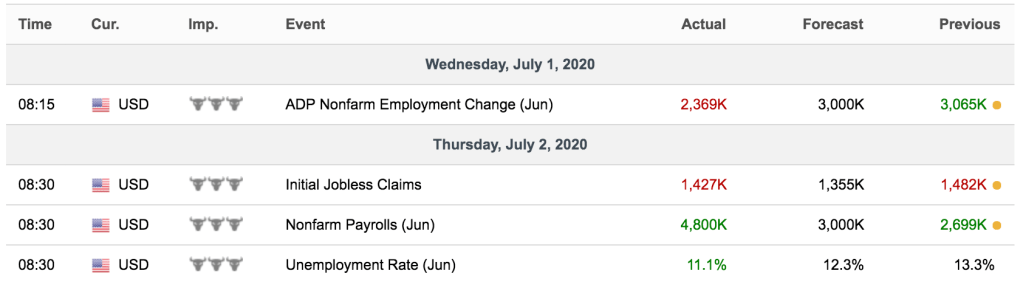

Over the past week, the incoming U.S. macro data largely confirmed a continuation of the existing slowdown narrative rather than a meaningful inflection. Backfilled BLS data showed October nonfarm payrolls down 105k, followed by a 64k rebound in November, while the unemployment rate rose to 4.6%, the highest level since 2021. We also saw underperformance in average hourly earnings for the month of November at 0.1%. This brought the year-over-year pace of nominal wage inflation back into the range that defined the pre-pandemic period. In terms of inflation, CPI surprised on the downside in dramatic manner. The year-over-year CPI print came in at just 2.7% and core CPI underperformed expectations at 2.6%. The fact that BLS simply marked some of the changes in OER and the rent components as zero subsequently skewed all of the inflation numbers lower.

Fed policy bias and the outlook for 2026 cuts

Looking ahead to 2026, the Federal Reserve’s policy bias appears increasingly clear: worries on hiring continuing to outweigh inflationary re-acceleration concerns. Employment has become the dominant variable, while inflation as it remains broadly contained, has moved down the list of immediate priorities. Looking forward, the distribution of risks around the jobs market still favor a less restrictive monetary policy stance. And even once Powell’s term is up and we have a new Fed chair, I am expecting that that bias will persist.

At the same time, the Fed prefers owning the front end of the yield curve to the long end of the curve. With government debt levels elevated and refinancing needs rising, maintaining control over short-term rates becomes as much a financial stability consideration as a macro one. Favoring rate cuts or at least resisting premature tightening helps ease debt servicing pressures across the public and private sectors, reinforcing the Fed’s preference for anchoring the front end even if longer-dated yields remain constrained by supply and term-premium dynamics.

equity market considerations for 2026

A more structural challenge sits beneath these near-term policy decisions. Global capital is being aggressively funneled into the AI ecosystem, from semiconductors to data infrastructure. While this investment wave has boosted productivity in select sectors, it has also crowded out employment and consumption growth in more traditional parts of the economy. As capital intensity rises and labor demand softens outside of tech, the Fed is increasingly confronted with data that point to uneven growth—strong at the top, fragile underneath.

This creates a feedback loop that complicates monetary policy. As earnings from major AI companies become macro events that markets trade around, the AI sector has grown too systemically important for policymakers to ignore. In that sense, AI risks becoming “too big to fail” from a market-stability perspective. A dovish fed, intended to support employment broadly, instead channel liquidity disproportionately toward AI and related assets, while offering limited relief to sectors facing structural job losses.

The implication is that, over shorter cycles, monetary policy becomes less effective at addressing real-economy imbalances. Liquidity supports asset prices more readily than it restores employment or consumption in displaced industries. This dynamic raises the risk of further asset-price inflation—even as underlying productivity gains remain uncertain. Heavy capital spending alone does not guarantee a sustained improvement in total factor productivity, and history suggests that such imbalances can eventually surface through higher volatility rather than smooth adjustments.

Against this backdrop, my outlook for 2026 rate cuts is shaped less by traditional inflation metrics and more by labor market fragility and financial stability considerations. The Fed’s easing bias is likely to persist, but its effectiveness may increasingly be expressed through asset prices rather than broad-based economic improvement, setting the stage for a market environment that appears stable on the surface, yet remains vulnerable to sharper dislocations down the road.

Political and fiscal uncertainty as a wildcard

One obvious concern to think about the year ahead is the degree to which the midterm election changes the behavior of the administration. Now we’re going into the midterms assuming that the Democrats take either the House or the Senate and end up with a divided government. This is very consistent with the political wins as well as a typical outcome during the second half of a given president’s presidency. What one would typically think is as a two-term president faces the last two years of his or her presidency with a divided Congress, they would effectively slip into the category of a lame duck or be a placeholder for the next administration. That would typically be characterized by no major initiatives on the legislative front and by a decrease in regulatory changes. Now, that’s a typical environment. Given the current administration’s behavior thus far, it wouldn’t be surprising to see when faced with a divided Congress, the administration tries to further expand the power of the executive branch. Now, whether that translates through to more executive orders and whether or not there’s a concerted effort on the part of the Supreme Court to limit some of the powers of the executive branch all remains to be seen. But, if nothing else, this represents a wild card that could find an expression in the equity market and therefore tighten financial conditions and perhaps more importantly, undermine the wealth effect and thereby cool both inflation and the real economy. According to J. Rangvid, based on current estimates of U.S. household exposure to equities, a 50% drawdown in U.S. equity markets would directly reduce consumer spending by approximately 3.8% and drag GDP growth lower by around 2.6 percentage points. Such a shock would be sufficient to fully offset the historical average growth rate of roughly 2.2%, thereby pushing the economy into a broad-based recession.

Dollar outlook and deficit monetization

Looking into 2026, the U.S. dollar faces growing structural headwinds rather than an obvious bullish catalyst. The Treasury has, for now, helped the Fed navigate a path toward effective deficit monetization, easing funding pressures but reducing the scarcity value of dollars at the margin. This dynamic, combined with a Fed that continues to prioritize labor market risks over inflation concerns, limits the upside for U.S. rates and weakens one of the dollar’s key sources of support.

At the same time, persistent fiscal deficits and heavy Treasury issuance are gradually weighing on sentiment toward dollar assets, even as global alternatives remain imperfect. While the dollar is unlikely to break down sharply given its reserve status, it is also difficult to make a convincing case for sustained strength. The most likely outcome for 2026 is continued range-bound trading with a mild downside bias, driven by easier financial conditions and ongoing deficit financing rather than a dramatic shift in global growth or risk appetite.